CCAR News

Property Managers: Let’s Connect!

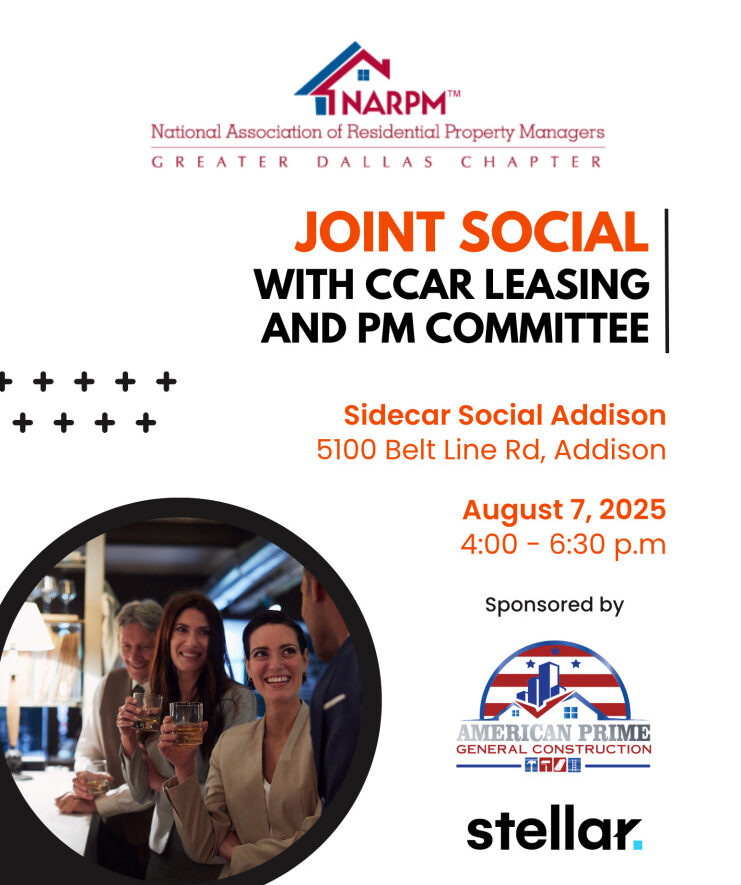

Property Managers: Let’s Connect! National Association of Residential Property Managers Greater Dallas Chapter and CCAR Leasing and Property Management Joint Social Join us for a fun evening at our Joint Social! Connect with fellow industry professionals, enjoy great conversations, and expand your network in a relaxed setting. Sidecar Social Addison August 7, 2025 Free Registration…

Read MoreProxy Voting is Underway: What You Need to Know

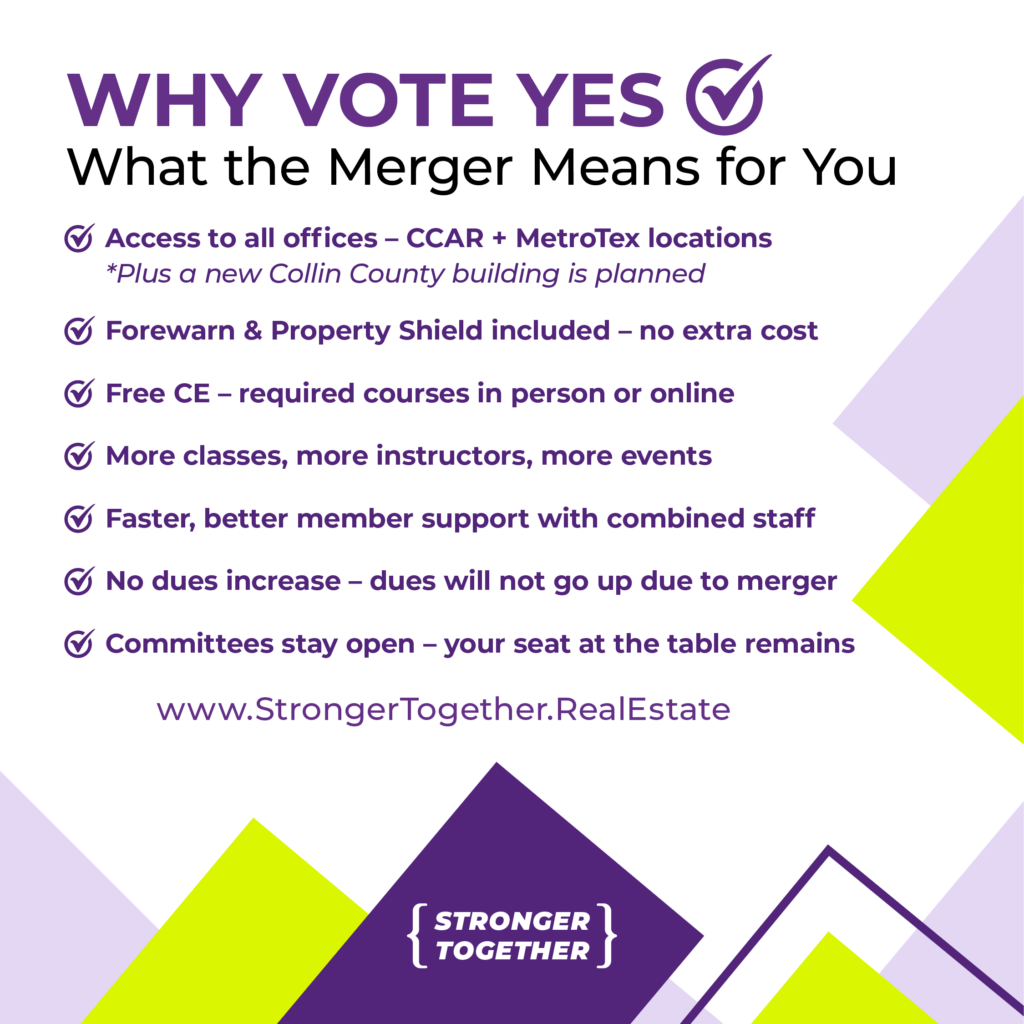

Proxy Voting is Underway: What You Need to Know The proxy voting period is currently open for our voting members to cast a proxy vote on the proposed merger between Collin County Area REALTORS® and the MetroTex Association of REALTORS®. On July 15, a reminder was sent to members who had not yet cast their…

Read MoreExplore International Real Estate: You’re Invited to an AMPI Congreso 2025 Kickoff Event

Explore International Real Estate: You’re Invited to an AMPI Congreso 2025 Kickoff Event Are you ready to take your real estate career across borders? MetroTex Association of REALTORS® has invited CCAR members to attend a special event designed to inform and inspire as they kick off the road to AMPI Congreso 2025—Mexico’s largest and most…

Read MoreAvoid the Pitfalls: Top 10 Mistakes in Property Management

Avoid the Pitfalls: Top 10 Mistakes in Property Management Are you involved in property management or considering diving in? The CCAR Property Management and Leasing Committee invites you to an insightful presentation you don’t want to miss: “Top 10 Mistakes in Property Management.” Join us as two experienced attorneys specializing in property management break down…

Read MoreUnlocking Hidden Inventory: How Understanding the Senior Market Can Create More Listings

Unlocking Hidden Inventory: How Understanding the Senior Market Can Create More Listings By: Kristy Osborn, CSA®, CDLP®, CMA™ Mortgage Equity Planner | Reverse Mortgage Division Lead Fairway Independent Mortgage Corp. and Member of CCAR’s Affiliate Committee In today’s low-inventory market, one group of homeowners is often overlooked: older adults. Many seniors want to stay in…

Read MoreMerger Vote Recommended to Membership by CCAR & MetroTex Board of Directors

Merger Vote Recommended to Membership by CCAR & MetroTex Board of Directors We are pleased to announce that after thorough due diligence, thoughtful discussion, and careful consideration, both the Collin County Area REALTORS® (CCAR) Board of Directors and MetroTex Association of REALTORS® (MetroTex) Board of Directors have voted to recommend a Plan of Merger between…

Read MoreThe Advocacy Alliance You Need to Know About

The Advocacy Alliance You Need to Know About If you’ve never heard of the American Property Owners Alliance (APOA), you’re not alone—but that’s exactly why you need to hear this episode. Marvin Jolly, Regional President and Past NAR RVP, joins the show to shed light on this nonprofit, nonpartisan organization that’s working behind the scenes…

Read MoreDoes It Really Matter Who My Inspector Is? (Spoiler: YES. Yes, it does.)

Does It Really Matter Who My Inspector Is? (Spoiler: YES. Yes, it does.) By: J.J. Petersen, TREC #9278, Forerunner Inspections and CCAR Affiliate Committee Member What if I told you that hiring the right home inspector could save you a cool $14,000 on your next home purchase? That’s not Monopoly money—that’s the national average of savings negotiated from a quality…

Read MoreSpring Surge in Listings Shifts Market Power to Homebuyers in Collin County

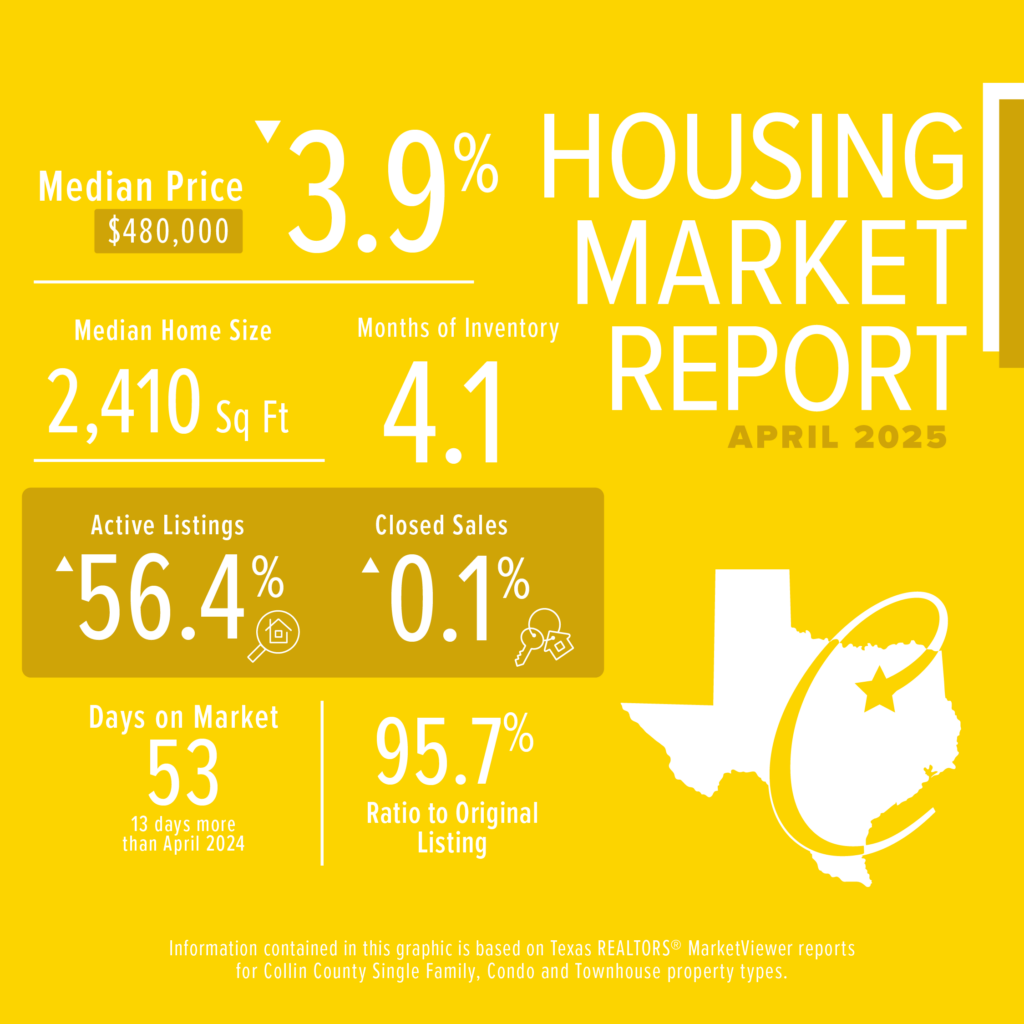

Spring Surge in Listings Shifts Market Power to Homebuyers in Collin County Collin County Area Realtors (CCAR) reports that increased new listings provided homebuyers significantly more choices and negotiating power, resulting in increased activity and lower prices in April. New listings in Collin County increased by 20.5% compared to April 2024 (2,945 vs. 2,445). This,…

Read MoreBeyond the Stigma: Prioritizing Mental Health in a Demanding Industry

Beyond the Stigma: Prioritizing Mental Health in a Demanding Industry May is Mental Health Awareness Month, and at Collin County Area REALTORS®, we’re having the conversations that matter most. In our latest Welcome to the Top podcast episode, CCAR President Jennifer Parker and COO Joanna Fernandez speak with CCAR team member Becky Pfaff, who brings…

Read More