Did you read last week's blog discussing appraisal do's and don'ts by Vaughn Kerkorian of Kerkorian Residential Appraisals?

We loved the feedback we received from our members who read the post! Your questions and engagement help us provide you with the information you want to know.

Many of you asked:

"Why is the buyer not the appraiser's client or the intended user of the appraisal report? Why is it not expected that the appraiser provide the buyer's agent or the buyer a copy of the appraisal report?

If the buyer/borrower is required by the lender to pay for the appraisal, how are they not the client and primary recipient of the appraisal report?"

Here is what Vaughn Kerkorian had to say:

"This is a good question that comes up in many training classes I conduct.

There is a misconception that just because one has a financial interest in the transaction that they therefore have a financial ownership in the transaction. Just because one pays for the appraisal to the lender/appraisal management company (AMC) does not make the individual(s) the appraiser's client. The borrower should be entitled to receive a copy of the appraisal report from the lender that ordered the report from the appraiser.

An appraisal report is ordered by the lender/AMC for a Federally Regulated Transaction (FRT) to determine an estimated opinion of value for a mortgage related transaction. The individual(s) that paid for the appraisal report are not the appraiser's client and therefore not the "client or intended user" of the report.

If an individual(s) ordered an appraisal report directly from the appraiser for a non-FRT such as estate planning, divorce, probate, etc. and have requested to be named the "client and/or intended user” they are then entitled to a copy of the appraisal report directly from the appraiser.

The key distinction is "who has directly engaged the appraiser for their services".

- In a purchase/refinance transaction (FRT), the lender orders the appraisal from the appraiser and compensates the appraiser directly, not the borrower.

- In a non-lender transaction (non-FRT), the individual(s) directly engages the appraiser for services rendered and directly compensates the appraiser. Therefore, they are entitled to receive a copy from the appraiser as the "client/intended user".

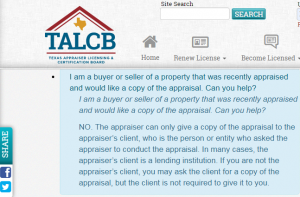

As a resource for agents to understand the appraisal client relationship, I have attached and linked this snippet from the TALCB website Q&A page:

Additional resources and avenues to learn more on the appraisal client relationship are:

* The Fannie Mae Selling Guide (this topic is covered in detail within the FNMA Selling Guide). Once downloaded, open the PDF document and perform a keyword search (i.e. - appraiser's client)

* Purchase a digital copy of USPAP (Uniform Standards Professional Appraisal Practice); perform a keyword search for a specific area of interest (i.e. - appraiser's client)

* Enroll & participate in basic appraisal training classes that are offered through CCAR or at an online training institution (may receive CE hours)

* Invite a local appraiser to your weekly sales meeting to discuss basic appraisal principles or for a Q&A session. If done as a Q&A, it would be best to have the questions provided to the appraiser prior to the meeting to be better prepared."

__________________________________

We hope that you found this information helpful! As always, let us know what kind of information your are seeking so that we can get it into your hands.